Because I'm a banker, I'm often asked about my opinions about the monetary policies that are being utilized in the United States and abroad. The question is generally summarized as, "With the Federal Reserve stimulating the money supply as they currently are, don't you think inflation is inevitable? And, given coming inflation, what do you think I should do with my savings?" Talk about some heavy-hitting questions ...

Before I continue, I must confess that just because I'm a banker doesn't mean that I receive a standard-issue crystal ball from Mr. Bernanke, so I really don't have any more concrete idea than you do about what the future holds. Sure, I may be exposed to some financial information that you don't see, but all that gives me is more data (which is not the same as information) off of which to form an opinion.

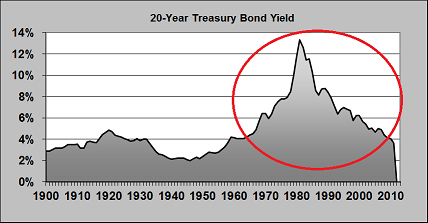

First, when people talk about interest rates rising, they are thinking of the rate cycles that have been common over their adult lifetimes. For most folks, this covers the portion of the chart (courtesy of Crestmont Research {www.crestmontresearch.com}) circled in red.

However, when you look at the part of the chart prior to the red circle, you will find that for the majority of the 20th century, interest rates were very close to where they are today - sometimes slightly higher, sometimes slightly lower. In fact, when you look at the 1920's (also known as the Roaring Twenties), you will find that rates were only slightly higher than today ... even in a time of significant economic growth and expansion.

So, what if rates are really returning to normal levels after the rate spike in the late 70's and early 80's? What should you do if you're wanting to maximize your return on dollars that you have in Astra Bank? I'd make two suggestions. The first is what I believe to be our best paying deposit in the bank - a 48-month Trade-a-Rate certificate of deposit (CD). With this CD, you earn a rate just slightly lower than our 48-month CD, but you have an option to adjust the CD rate once during the term of the CD. Accordingly, if rates go up, you still have a feature in the CD that allows you to take advantage of rising rates. Just so you know, we also have 24-month and 36-month Trade-a-Rate CD's.

The second suggestion is to build a "ladder" of CD's. What do I mean by that? Instead of having one large CD, you have several CD's that mature over the investment period. As an example, instead of one CD of $40,000 that matures every four years, you have 4 CD's of $10,000 with one maturing each year over the four-year period. This strategy positions you to better take advantage of rate changes - especially when you anticipate that rates may rise. For the best of all possible worlds, you can build a ladder of Trade-a-Rate CD's!

Does this answer the question about inflation? No, but it provides a solution for how to maximize earnings on your deposits in a rate environment that hasn't been seen since the 1950's. If you need assistance with maximizing earnings on your deposits, please come see us. We look forward to helping you turn your deposit dollars into fulfilled dreams!